Independent audit, internal audit, and external audit are overlapping terminologies that all serve to achieve the regulated standard accepted in all areas of accounting profession (Jasmani & Salleh, 2014).

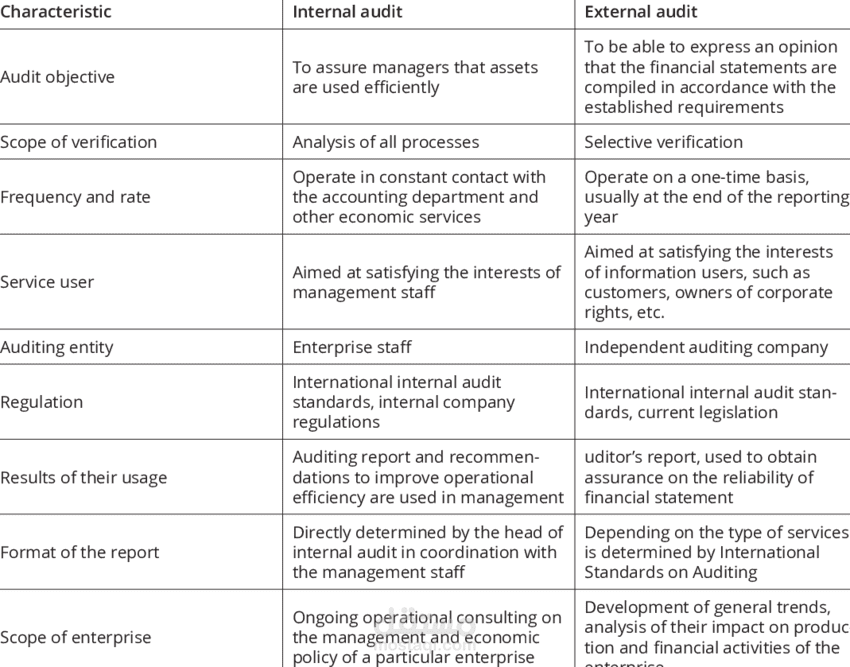

While the independent audit is regarded as an examination that evaluates the financial statements conducted by an external auditor, in preparation for providing the stakeholders, such as shareholders and creditors, with the necessary knowledge regarding the financial reporting transparency, internal audit, on the other hand, comes to complement shortfalls, trying to maintain the risk management effectiveness and governance processes integrity, which means that internal auditors are responsible for conducting an operational review, identifying areas for improvement, and providing recommendations to develop the internal controls (Green et al., 2011).

Contrary to internal audit, external audit is conventionally conducted by an independent accounting firm (Choi et al., 2014). The primary responsibility of an external auditor is to express an opinion on the financial statement fairness and to assess whether the financial statements comply with the applicable accounting standards and regulatory requirements (Bradbury et al., 2011). The three forms of audits serve distinct yet vital purposes in ensuring the financial reporting trustworthiness and accuracy, as independent audit offers an external perspective, internal audit discusses the internal processes and inspects the data validity and consistency, and the external audit provides assurance to external stakeholders. Understanding the nuances of these auditing practices is essential for maintaining transparency and accountability in the business world today.

Auditing analysis serves as a valuable tool for extracting meaningful insights from audit reports and identifying recurring issues.

Through incorporating auditing analysis into the operational processes, organizations can gain a deeper understanding of the underlying trends and patterns within financial and operational data. The complexity of audit processes necessitates a comprehensive approach that embraces the audit data, leveraging the nuanced patterns and anomalies that may have significant implications for the company’s risk management strategies.

The previous studies surrounding independent, internal, and external audits underscored the auditing functions’ critical role in extracting valuable insights and understanding the multifaceted nature beyond data. By delving into such previous studies and leveraging thematic analysis, organizations can enhance the auditing processes’ effectiveness and drive informed decision-making.

When it comes to financial transparency and regulatory compliance, auditing functions perform a vital role represented in independent audit, internal audit, and external audit, which often work hand in hand to ensure the organizational financial statement integrity (Zhang et al., 2007). In an elaborate research study, Broberg identified the mutual themes that connect these three types of audits, and embark on a qualitative analysis journey to unearth the common threads, which bind independent audit, internal audit, and external audit all together (Broberg et al., 2013). Another study began its hypothetical activity by understanding what independent audit entails, clarifying that independent audit refers to the process of evaluating an organization's financial statements through the efforts undertaken by the external auditors, who offer unbiased assurance (Gold et al., 2020). This auditing function is crucial, since it provides the stakeholders with confidence and trust in the reported financial information procedures.

| اسم المستقل | فلتراسلني Bulchritudemind At Live Dot Co Dot Uk س. |

| عدد الإعجابات | 0 |

| عدد المشاهدات | 52 |

| تاريخ الإضافة |