Hedging Exchange Rate Volatility with Financial Derivatives(Financial Risk Management)

تفاصيل العمل

This graduation project provides an in-depth financial and strategic analysis of exchange rate volatility and the role of financial derivatives in hedging currency risk.

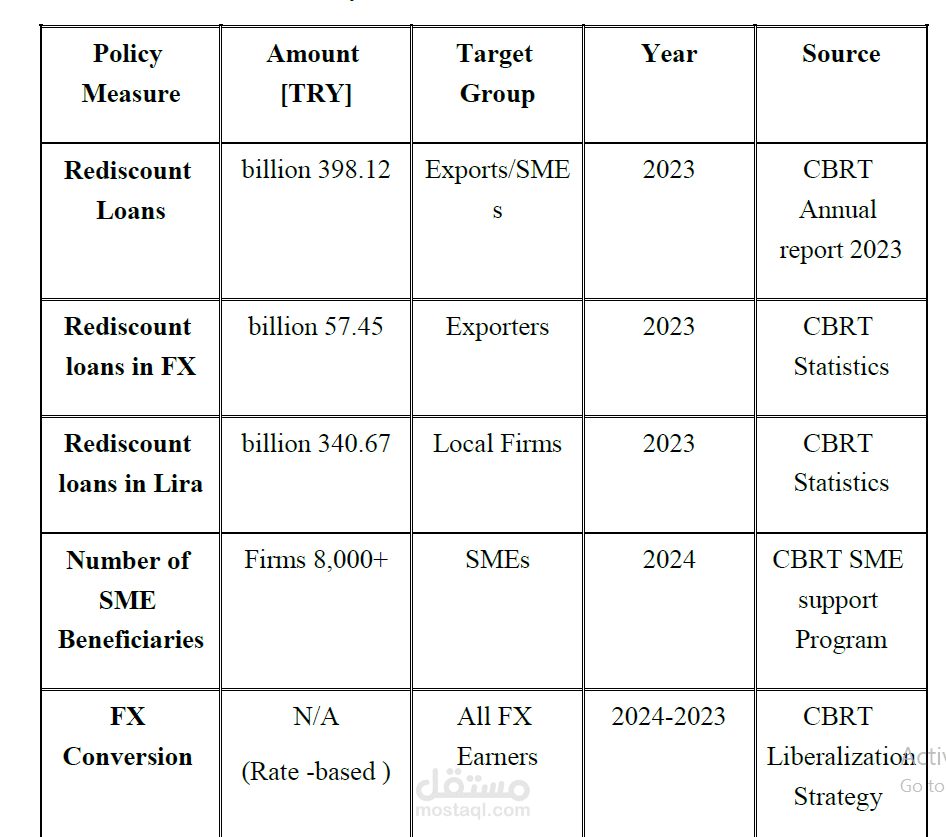

The study examines the 2018 Turkish Lira crisis and compares it with the 2022–2024 Egyptian Pound crisis, analyzing their macroeconomic causes, monetary policy responses, and sectoral impacts.

A comprehensive financial analysis was conducted on major corporations including Arçelik and Türk Telekom in Turkey, and Juhayna, Edita, Orascom Construction, and Abu Qir Fertilizers in Egypt.

The project evaluates hedging effectiveness using forwards, futures, swaps, and options, supported by real financial statements, cash flow analysis, profitability ratios, and risk exposure assessment.

The study concludes with strategic recommendations for policymakers and corporations to enhance financial stability through derivative-based risk management frameworks.