مبحث أدبي وعلمي في آن واحد حائز تقييم A+ (جامعة Harvard)

تفاصيل العمل

Brief Introduction:

Modern technology impacted the way businesses operate (Pratama et al., 2023), particularly in the realm of administrative accounting and performance management (Nurjanna et al., 2023).

The escalating digitalization of administrative accounting and performance management paved the way for increased efficient and effective processes (Kovalevska et al., 2024), ultimately shaping the industry landscape (Mansoor et al., 2024). This paper penetrates the digitalization processing impact on administrative accounting and performance management, providing valuable insights that clarify the distinctive power, which recent technologies possess, especially in the business domain.

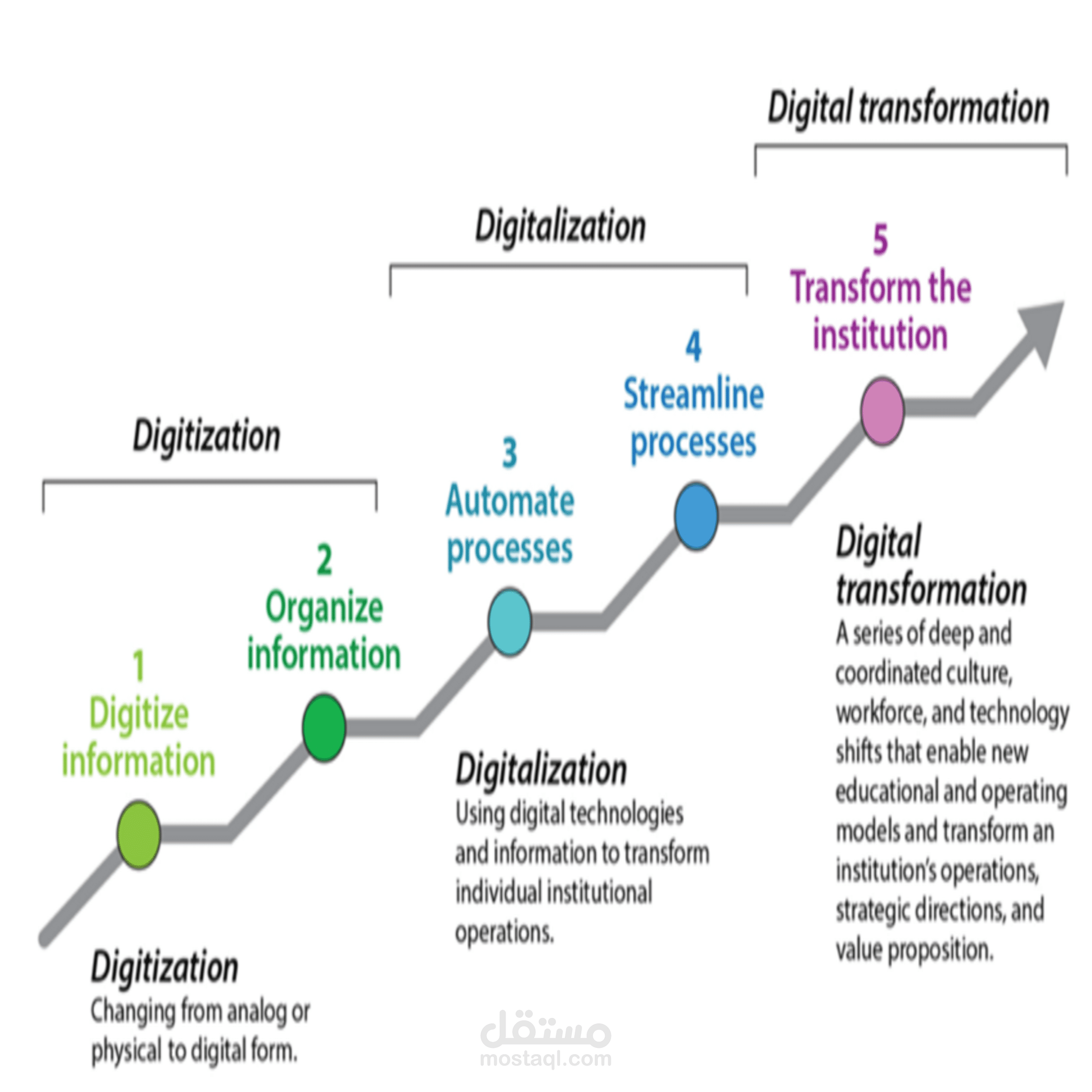

As known, in today's fast-paced digital world, the accounting industry underwent an apparently significant mutation that changed the recognized practices and familiar methods (Gnatiuk et al., 2023), resulting in improved decision-making techniques (Platov et al., 2023). In this investigative research study, the data explored the evolution of administrative accounting and performance management, analyzing the conceptual outputs derived from the accounting software, cloud computing, and AI-assisted applications, which streamlined executive processes, allowing businesses to access real-time evidence and to also generate accurate financial reports. This indicates that most standard and conventional accounting practices, involving manual data entry and filed records, are gradually being replaced by digital technologies in order to automate ordinary tasks and to also enhance data security and regulatory compliance.

Methodology Summary

The study employed an exactly quantitative research approach to analyze the digitalization surge and examine the business boom, which administrative accounting and performance management witness today.

The study selected diverse data sources that enriched the research process and explored different facets of digitalization activities. Primary data sources such as financial statements, transaction records, and performance metrics also offered firsthand insights regarding the organizational practices. Secondary data sources, including scholarly articles, industry reports, and government publications, provided valuable context and theoretical frameworks for analysis. Through utilizing data from an obviously diverse range of companies across various industries, the researcher explored the key metrics and indicators to gauge the digital technologies that eradicated the usual accounting practices and replace them with dynamic means. Through rigorous statistical analysis, the study revealed the specific ways that shaped the digitalization approaches, which, in turn, shaped the future of financial reporting and performance evaluation.