Backtesting Trading Strategy

تفاصيل العمل

Backtesting Strategy

Background:

Algorithmic trading involves using computer algorithms to execute trading strategies. A crucial step in this process is backtesting, where historical data is used to simulate how a given strategy would have performed in the past. It's a powerful tool for refining and validating trading ideas.

What I Did:

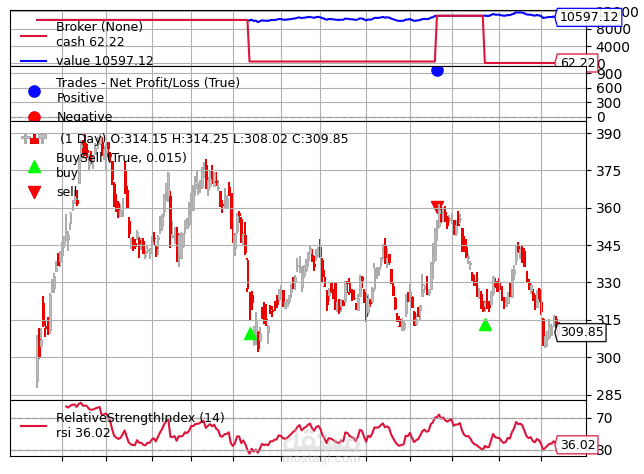

In this project, I focused on Relative Strength Index (RSI), a popular momentum indicator. I used Python and Backtrader to implement an RSI-based trading strategy. The strategy buys when RSI is below a certain threshold (indicating oversold conditions) and sells when RSI is above another threshold (indicating overbought conditions).

Key Steps:

Data Retrieval: Fetched historical stock data using yfinance.

Strategy Implementation: Coded an RSI strategy using Backtrader.

Backtesting: Simulated the strategy over historical data to evaluate its performance.

Results Analysis: Checked the buy/sell signals and assessed the strategy's profitability.

Why Backtesting Matters:

Backtesting allows traders and developers to assess the viability of a strategy before risking real money. It helps in identifying potential flaws, optimizing parameters, and gaining confidence in the strategy's effectiveness.

Takeaway:

Whether you're a seasoned trader or a curious learner like me, backtesting is a valuable skill in the world of algorithmic trading. It's a journey of exploration, analysis, and continuous improvement.